Per-Day Costs

(FY27 budget, function 1050, excluding OoC pass-through)

(Linn County and Henry County contracts, 2024–25)

Linn County charged U.S. Marshals $86–$140/day for the same beds

No pro-forma operating budget for the new facility has been published

The $315/day in-house figure

The FY27 Total Expenses Budget breaks out the Sheriff's Office by function code. Function 1050 is the jail. Its total is $7,186,029, which includes $800,000 for SC349 — Inmate Housing, Out of County. That line is a pass-through to other counties, not a cost of operating the Johnson County jail. Removing it yields an in-facility operating cost of $6,386,029.

Divided by the FY26 partial in-house ADP of 55.62 × 365 days: $6,386,029 ÷ 20,302 = ~$315/day per person.

Personnel and benefits account for 89% of that cost (FY27 Total Expenses Budget, Function 1050: $5,689,901 personnel+benefits ÷ $6,386,029 in-facility cost).

Show FY27 Function 1050 line-item budget

| Line item | FY27 budget |

|---|---|

| SC100 Salaries of Regular Employees | $3,708,064 |

| SC101 Wages of Temporary & Part-time | $120,739 |

| SC104 Overtime & Shift Pay | $173,710 |

| SC111 IPERS (pension) | $424,813 |

| SC113 Employee Group Health Insurance | $912,392 |

| SC114 Allowances to Employees | $11,520 |

| SC117 Other Benefit Programs | $45,760 |

| Social Security | $292,903 |

| Total personnel and benefits | ~$5,689,901 |

| SC230 Commodities — Food & Provisions | $331,000 |

| SC231 Clothing & Dry Goods | $11,000 |

| SC234 Kitchen Supplies | $6,500 |

| SC291 Medical & Laboratory Supplies | $5,000 |

| SC294 Wearing Apparel & Uniforms | $30,000 |

| SC302 Primary Treatment | $18,000 |

| SC306 Prescription Medication/Vaccines | $80,000 |

| SC349 Inmate Housing — Out of County | $800,000 |

| SC378 Contracted Coordination Services | $13,000 |

| SC413 Mileage & Other Travel Expenses | $47,100 |

| SC422 Educational & Training Services | $84,625 |

| SC447 Repair & Maintenance — Misc. | $16,041 |

| SC453 Rentals — Office Equipment | $5,137 |

| SC634 Household & Institutional | $4,200 |

| SC636 Office Equipment & Furniture | $6,650 |

| Other misc. | ~$194,875 (est.) |

| Total non-personnel | ~$1,496,128 |

| Function 1050 Total | $7,186,029 |

Source: JoCo FY27 Total Expenses Budget, CC08 Sheriff, Function 1050 (Jail). SC349 ($800,000) excluded from the in-facility per-diem calculation as an intergovernmental pass-through.

The 65-bed cap in historical context

Sheriff Kunkel stated in May 2024 that he caps in-house population at approximately 65. The monthly control sheets support two readings of that cap. Pre-COVID stable years (FY17–FY19) show an average in-house ADP of approximately 62.2/day — just below 65, consistent with a cap that was being approached but not exceeded. Post-COVID stable years (FY22–FY26 partial) show an average of approximately 55.5/day — roughly 10 below the stated cap. The two readings are: (a) the cap is unchanged at 65 and post-COVID demand simply dropped; or (b) the cap was tightened de facto after COVID, and the 65 figure reflects an earlier, looser practice. Distinguishing between them requires daily peak data. The monthly control sheets report monthly averages only; daily peaks are not published.

The $60/day out-of-county rate

Johnson County pays $60/day to Linn County (Cedar Rapids) under a 2024 agreement with a 4% annual escalator, and $60/day to Henry County from FY2025 (up from $50/day). The rates paid to Cedar, Lee, and Washington counties are not publicly reported.

The $60/day figure is a transfer rate between counties — what intergovernmental negotiation produced — not necessarily a measure of what it costs to run a jail. Linn County previously charged the U.S. Marshals Service $86–$140/day for the same beds (The Gazette, 2024).

Comparing Johnson County's average in-house cost ($315/day) directly to the $60 transfer rate conflates a fully-loaded average cost with a sub-cost intergovernmental rate. The two figures are not measuring the same thing.

The $960K standing budget — the OoC pressure point is partly an artifact

The OoC budget line has been static at $960,000 across every published year through FY26. Sheriff Kunkel confirmed at his November 2024 budget presentation:

Standing budgeted amount of $960,000 — in place before I came into office. This number can fluctuate over time, always kept budgeted amount static in case of emergency.

Kunkel took office January 2017. FY23–FY25 actuals were $331K–$440K — between 35% and 46% of budget. The FY27 line drops to $800K with no published justification. The "$800K projected OoC pressure" framing in bond-justification materials uses a budgeted number two-to-three times what the County has actually spent in any year since 2015. Actual OoC spending peaked in calendar year 2010 at $1.89M and has trended downward since 2015.

Show FY17–FY27 out-of-county housing history

| FY | Actual spend | OoC ADP | Implied per-diem |

|---|---|---|---|

| FY17 | $451,085 | 23.52 | ~$52/day |

| FY18 | $827,105 | 39.73 | ~$57/day |

| FY19 | $648,750 | 36.54 | ~$49/day |

| FY20 | $531,055 | 28.89 | ~$50/day |

| FY21 | $302,155 | 16.35 | ~$51/day |

| FY22 | $459,205 | 27.28 | ~$46/day |

| FY23 | $326,805 | 18.28 | ~$49/day |

| FY24 | $303,120 | 16.98 | ~$49/day |

| FY25 | $440,380 | 21.85 | ~$55/day |

| FY26 (partial, 6 mo) | $240,319 | 24.49 | ~$54/day |

| FY27 (budgeted) | $800,000 | — | — |

Source: Johnson County Sheriff's Office control sheets (FY17–FY26 partial). Implied per-diem = actual spend ÷ (OoC ADP × 365). FY27 is budgeted, not actual. The implied per-diem rose from ~$46–$52 (FY17–FY23) to ~$54–$55 (FY24–FY26), consistent with contract rate increases. FY27 budget of $800K is ~2.6× the FY24 actual.

Comparison table

| Housing type | Rate | Source |

|---|---|---|

| JoCo in-house (FY27 budget basis) | ~$315/day | JoCo FY27 budget, function 1050 |

| JoCo pays Linn County | $60/day | 2024 contract (4% annual escalator) |

| JoCo pays Henry County | $60/day | FY2025 contract |

| Linn County charged U.S. Marshals (prior) | $86–$140/day | The Gazette, 2024 |

| Iowa state prisons (avg) † | ~$116/day | Iowa Legislature FY data |

† Iowa state prisons house longer-term sentenced incarcerated people with different programming, medical, and security cost structures than county jails. The $116/day figure is included as a reference benchmark only and is not directly comparable to county jail operating cost.

The Sheriff is already cutting per-position cost via civilianization — independent of any new facility

Job Bulletin #00852 (Detention Officer, posted May 5, 2025) lists the wage at $29.68/hour — approximately $61,700 base salary. The position is female-only under Iowa Code §356.5 BFOQ. In his FY26 and FY27 budget planning forms, Sheriff Kunkel documented the per-position savings from civilianizing Deputy Sheriff positions through attrition:

We will continue operating under the new jail staffing model by filling open deputy sheriff positions with civilian detention officers. This is saving an estimated $14,000 in salary and benefits plus an additional $10,000+ in ILEA expenses per position.

Total documented savings: ~$24,000/year per civilianized position. This is happening now, independent of any bond-funded facility. Two implications: (1) the elevated per-diem cost of the existing jail is in part a function of the staffing model, which the Sheriff acknowledges can be tightened; (2) any bond-campaign framing that treats the current operating cost as fixed and inflated by aging infrastructure ignores cost reductions the Sheriff has already identified and is implementing.

ADP in context: Johnson County vs. population

Normalizing ADP to county population helps contextualize the facility's actual use. Using U.S. Census Bureau Vintage 2024 Population Estimates for Johnson County (July 1 of the fiscal year start) and control-sheet ADP:

| FY | JoCo population (July 1) | In-house ADP | In-house per 100K | Total in-custody ADP | Total per 100K |

|---|---|---|---|---|---|

| FY22 | 155,035 | 50.99 | ~33 | 85.00 | ~55 |

| FY23 | 156,915 | 57.21 | ~36 | 81.71 | ~52 |

| FY24 | 157,528 | 56.82 | ~36 | 81.15 | ~52 |

| FY25 | 160,080 | 56.70 | ~35 | 84.08 | ~53 |

Population: U.S. Census Bureau, Population Estimates Program (PEP) Vintage 2024; July 1 estimates for Johnson County, Iowa (FIPS 19103). 2021–2023 from Vintage 2024 PEP; 2024 = 160,080 (Census QuickFacts). ADP from Johnson County Sheriff's Office control sheets. Total in-custody includes in-house + out-of-county housed + electronic monitor. FY21 (COVID recovery year) excluded; in-house ADP of 34.78 would yield ~22/100K. Table ends at FY25 because the Sheriff's dashboard "12 Month Trend" (Jun 2025–May 2026) is a rolling window straddling FY25 and FY26 — not a full fiscal year. See the Overview ADP section for the most recent rolling trend figures.

Capital Costs

The Sheriff's Office and Jail Bond per the May 20, 2026 MCIP totals $96M for the combined jail and Sheriff's Office facility. The $16M affordable-housing component is financed through a separate essential-purpose bond (Resolution 04-23-26-02, April 23, 2026) and is not included in the $96M. Because the $96M covers both the jail and the SO, dividing the full bond by jail beds overstates per-bed cost. Shive-Hattery Vol. I (August 2024) split the combined facility at ~61% jail / ~39% law enforcement by cost; Sheriff Kunkel has publicly characterized the jail as approximately half the project. Per-bed cost varies substantially depending on which share is used:

| Scenario | Beds | Capital basis | Cost per bed |

|---|---|---|---|

| Full $96M ÷ 120 built-out beds (upper bound) | 120 | $96M | ~$800K/bed |

| Full $96M ÷ 140 beds (incl. 20 shelled) | 140 | $96M | ~$686K/bed |

| 61% jail share (Vol I split) ÷ 120 beds | 120 | ~$58.6M | ~$488K/bed |

| 50% jail share (Sheriff Kunkel) ÷ 120 beds | 120 | ~$48M | ~$400K/bed |

| Jail-only (Shive-Hattery Vol I 2024 estimate) | 120 | ~$48.88M | ~$407K/bed |

Confirmed post-2022 comparables (all combined Sheriff's Office + jail unless noted):

| Facility | Built beds | Cost | Per bed | Notes |

|---|---|---|---|---|

| Warrick County, IN (opened 2026) | ~300 | ~$50M final | ~$167K | Scale: ~2.5× JoCo's 120; per-bed cost falls with size. Source: WFIE/14News, June 24, 2026. |

| Kewaunee County, WI (2023) | 58 (85 expandable) | $25.6M approved; ~$33M rebid | ~$441K–$569K | Includes jail + 911/dispatch + Sheriff's Office (40,500 SF). Rebid after inflation. Source: Kewaunee County Star-News; WBAY, Aug 2023. |

| Otsego County, NY (2025 estimate) | 96 | $64.5M total / $53.7M construction | $672K total / $559K construction | Maximum-security; carries higher cost than standard county jail. |

| JoCo proposed (jail-only component) | 120 | ~$48.88M (Shive-Hattery 2024) | ~$407K | Does not include Sheriff's Office. Full $96M bond ÷ 120 beds = $800K. |

Per-bed cost is strongly size-driven: Warrick at ~300 beds comes in at ~$167K/bed; Kewaunee at 58 beds reaches ~$569K/bed; Otsego at 96 beds (maximum-security) reaches $672K/bed. JoCo's jail-only component at ~$407K/bed sits between Kewaunee and Warrick, adjusted for scale. The full $96M ÷ 120 = $800K figure includes the Sheriff's Office building and is not directly comparable to jail-only per-bed figures. Per-bed cost falls if the 20 shelled beds are included or if the facility runs at higher occupancy. All comparables should be verified against primary construction documents.

Annualized capital cost per person per day

At $96M (MCIP bond figure) over 10 years at 4.5%, debt service is ~$12.13M/year (PMT = $96M × 0.045 × 1.045¹⁰ / (1.045¹⁰ − 1); 10-year term per June 10, 2026 work session). That debt service, divided across occupied beds, produces the following capital cost per person per day — before any operating costs:

| Occupancy | Prisoners/day | CapEx per person per day |

|---|---|---|

| Current in-house ADP | 56 | ~$594/day |

| Full managed ADP (incl. OoC and EM) | 84 | ~$396/day |

| Full 120-bed capacity | 120 | ~$277/day |

The Shive-Hattery Supplemental Life Cycle Cost Analysis states that the Build New scenario operates with 24 staff positions but does not publish a pro-forma operating budget — no per-person or annual operating cost figure appears in the document. The only primary-source-grounded all-in figure available is debt service plus current JoCo operating cost scaled to 84 ADP: $6.386M ÷ (84 × 365) = ~$208/day operating + ~$396/day debt service = ~$604/day.

This is a reference point, not a projection: it asks "what would today's operating cost per person be at the new facility's expected population?" Shive-Hattery's Build New scenario specifies 24 FTE, compared to the current jail's staffing embedded in the $5.69M personnel budget. Whether 24 FTE at a modern direct-supervision facility produces lower per-person operating cost than today cannot be evaluated without a published operating pro-forma. That document has not been released.

The debt service figure is fixed — it does not change with occupancy. The per-person share of that fixed cost falls as more people occupy the facility:

| Occupancy | ADP | Debt service/p/day |

|---|---|---|

| Current operational cap | 65 | ~$511/day |

| Current total managed ADP | 84 | ~$396/day |

| Initial built-out capacity | 120 | ~$277/day |

Debt service calculated as $12.13M/year ($96M at 4.5%, 10-year level amortization; term per June 10, 2026 work session) divided by occupancy × 365. The 65-bed "operational capacity" is the Sheriff's figure used by Shive-Hattery; its basis has not been established in any published document (see Section 1).

The $69.4M Savings Claim

The $69.4M figure comes from Shive-Hattery's Supplemental Life Cycle Cost Analysis (July 2024). It is the difference between two projected 20-year scenarios:

- Build New: construct the 140-bed jail plus Sheriff's Office ($79.75M combined / $48.88M jail-only), operate with 24 staff.

- "Do Nothing" (forced-closure scenario): close the existing jail, build a holding facility ($13.6M–$50M), house all people held out of county at $60/day plus 2% annual inflation, operate an 18–30 staff transport unit.

Shive-Hattery's "Do Nothing" label describes a forced-closure scenario in which the existing jail is taken offline and all people held out-of-county. The County has not made that closure decision, no regulatory order requires it, and the existing jail's State Inspector record shows zero non-compliance items in both 2025 and 2026. This is a forced-closure comparison, not a comparison to the current status quo.

The actual annual OoC spend is $440K–$800K. The forced-closure scenario projects $4.8M/year on average. That gap is not because OoC rates are wrong — it is because the scenario assumes all ~83 current people are transferred out, not just the ~22 who are currently housed elsewhere.

How the savings figure changes with the actual bond amount

Shive-Hattery's Life Cycle Cost Analysis contains no debt service at all — no term, no interest rate. The $69.4M savings is a comparison of lump-sum capital plus 20-year operating costs. Once any financing is added, the savings collapse. The table below uses 10-year level-payment amortization at 4.5% (the term confirmed June 10, 2026; rate is an estimate) with the operating component derived from Shive-Hattery's $212M anchor row: $212M − $48.88M lump-sum capital = ~$163M operating over 20 years.

| Capital basis | Build New 20-yr total | Forced-closure 20-yr total | Difference |

|---|---|---|---|

| $48.88M (Shive-Hattery Vol I, anchor) | ~$225M | ~$282M | Forced-closure +$57M |

| $79.75M (Shive-Hattery Supplemental) | ~$264M | ~$282M | Forced-closure +$18M |

| $83M (facility only) | ~$268M | ~$282M | Forced-closure +$14M |

| $96M (MCIP bond figure) | ~$284M | ~$282M | Build New +$2M (roughly break-even) |

Build New 20-yr total = (capital basis × 10-yr PMT factor 0.12638 × 10 years) + $163M operating. Forced-closure total held at Shive-Hattery's stated $282M. The $96M bond covers jail + Sheriff's Office; the $48.88M anchor is jail-only — the scopes do not cleanly align, so the exact break-even figure carries uncertainty in both directions. Under 20-year amortization (the assumption used in all prior public presentations), the same table would show Build New at $96M ≈ $311M — about $29M more expensive than forced-closure.

The "$69.4M savings" claim is entirely an artifact of using the Vol I $48.88M planning estimate as the capital basis, and of omitting financing costs entirely. At the actual $96M MCIP bond figure, once any interest is counted, Build New and the forced-closure scenario are roughly the same cost over 20 years. The 10-year term chosen June 10 produces less total interest (~$25M) than a 20-year term (~$52M would), so the 10-year case lands marginally more favorably in the life-cycle frame — but not by enough to restore a meaningful savings margin.

The undisclosed population assumption

The forced-closure scenario projects $89.3M in per-diem costs over 20 years. The document states three inputs for this figure: 83 people/day, $60/day starting rate, and 2% annual inflation. Those three inputs do not produce $89.3M — they produce approximately $44.7M. At least one input must differ from what is stated. There are three possible readings:

| If this variable is adjusted… | …it must equal | Notes |

|---|---|---|

| Population (rate and inflation fixed at stated values) | ~170 people/day | Double the stated 83/day; exceeds Build New design maximum of 140 |

| Average per-diem rate (population fixed at 83/day) | ~$147/day average over 20 years | Requires rates roughly 2× the Linn agreement; or an inflation assumption near 8.5%/year rather than stated 2% |

| Inflation rate (population and starting rate fixed) | ~8.5%/year | More than four times the stated 2% assumption |

The document does not disclose which variable was adjusted or why. All three readings require an undisclosed departure from the stated inputs.

The population reading (170/day) has an additional internal inconsistency: Shive-Hattery sized the Build New facility for a maximum of 140 people (120 permanent beds + 20 flexible). The same consultant cannot simultaneously project 170/day future need for the forced-closure scenario and design Build New for a 140-bed maximum — the facility would be undersized on day one of its intended use. If 170/day is the correct population assumption, the ~$284M Build New 20-year total at $96M is still understated, because the facility would require a second expansion before the 20-year period ends.

If the stated 83/day population is correct instead, the forced-closure scenario's 20-year per-diem is approximately $44.7M — and the forced-closure 20-year total falls from ~$282M to ~$237M. At the MCIP bond figure of $96M, Build New (~$284M) would be approximately $47M more expensive than that corrected forced-closure total over 20 years.

Debt Service

Johnson County's existing bonds are nearly paid off. The FY27 Tax Calculation Worksheet shows the Debt Service Fund (Fund 65) with FY27 tentative revenues of $36,038 — effectively zero. The county is at or near the end of its current bond obligations.

The June 10, 2026 Board of Supervisors work session was the first time a repayment term appeared on the public record for this bond. Chair Jon Green, presenting Finance Director Dana Aschenbrenner 's calculation, stated that the $107/$100K tax figure is for a 10-year repayment schedule, and explained: "This is a large borrowing and given the uncertainty in the world, it is the judgment of the finance folks that we will receive more favorable terms on a 10-year repayment schedule." All prior Shive-Hattery reports and board presentations used a 20-year assumption — or no stated term at all.

At $96M, 4.5%, 10 years: PMT = $96M × 0.045 × 1.045¹⁰ ÷ (1.045¹⁰ − 1) ≈ $12.13M/yr; total payments $121.3M; interest $25.3M. The 20-year equivalent would be ~$7.38M/yr with total interest ~$51.6M. Choosing 10 years raises the annual levy by ~65% but saves ~$26M in lifetime interest and retires the debt by roughly 2036–2037.

The FY27–FY31 MCIP (May 20, 2026) lists the Sheriff's Office and Jail Bond at $96M total. The $16M affordable-housing component is financed through a separate essential-purpose bond (Resolution 04-23-26-02, April 23, 2026) that does not require voter approval and is not on the ballot. The June 10 work session confirmed the ballot scope as jail + Sheriff's Office only; formal adoption of the bond resolution was deferred at the July 2, 2026 formal meeting; the deadline to adopt is August 26, 2026.

| Bond amount | Rate | Annual payment | 10-yr total |

|---|---|---|---|

| $48.88M (Shive-Hattery Vol I basis) | 4.5% | $6.18M/yr | $61.8M |

| $79.75M (Shive-Hattery Supplemental basis) | 4.5% | $10.07M/yr | $100.7M |

| $83M (facility only) | 4.5% | $10.49M/yr | $104.9M |

| $96M (MCIP bond figure, 4.5%) | 4.5% | $12.13M/yr | $121.3M |

| $96M (4.0%) | 4.0% | $11.84M/yr | $118.4M |

| $96M (5.0%) | 5.0% | $12.43M/yr | $124.3M |

The gap between Shive-Hattery's Supplemental basis ($79.75M) and the MCIP bond figure ($96M) is $16.25M in principal and approximately $20.6M in additional 10-year debt service at 4.5%. Neither Shive-Hattery document contains any stated term or rate; the gap between their capital estimate and the actual bond ask was not addressed in the life-cycle analysis.

The $16M affordable-housing component is financed through a separate essential-purpose bond (Resolution 04-23-26-02) and is not within the $96M GO bond amount.

Three things the 10-year choice deserves scrutiny on

The board's public-finance rationale is real — shorter term, less interest, debt retired sooner, less long-horizon rate risk. But three aspects warrant examination:

- Front-loading and intergenerational mismatch. Standard municipal practice matches bond term to asset life. A jail and Sheriff's Office built in 2027–2029 will be in service for 40+ years. Financing it over 10 years concentrates the full capital cost on taxpayers of the current decade for an asset four decades of residents will use. Long terms save current payers money; short terms save future interest but shift the burden onto the present.

- The levy shock. The county's debt-service fund is at near-zero today (~$36K, FY27 Worksheet). A 10-year schedule drops a ~$12.1M/yr levy all at once. The FY27 debt-service taxable valuation is ~$11.81B; that implies a levy of roughly $1.07/$1,000 — a levy the county has not carried for years.

- The last-minute problem. The $107/$100K tax figure — now confirmed in the July 2, 2026 resolution/notice (Granicus clip 3693, Res. 07-02-26) — was first stated publicly on June 10, 2026, well before the ballot language was finalized. CSSI's survey instrument (October 2025) named no dollar figure at all; the focus groups reacted to an $80M total with no annual tax number attached. Whatever public support the research measured, it was measured before voters had the actual tax figure. The figure they are being asked to approve — $321/yr on a $300,000 home for 10 years — was not the figure in front of the public when opinion was gauged.

The Land Is Being Bought Outside the Bond

purchased July 2, 2026, 5-0

(acreage pending survey/replat; total is approximate)

(ballot language not yet adopted; deadline Aug. 26, 2026)

On July 2, 2026, the Board of Supervisors voted 5-0 to approve a definitive purchase agreement for approximately 35 acres at the SW corner of IWV Road SW & Slothower Road, inside Iowa City limits. The price is $60,000 per acre of gross land area — approximately $2.1M total, with the exact figure to be set once a survey and replat record the final acreage. The purchase is funded entirely from County reserves; it is not part of the $96M bond.

The ballot proposition names "acquiring land"

The draft ballot proposition in the July 2 packet (Res. 07-02-26) would authorize bonds "for the purpose of acquiring land and constructing, equipping and furnishing a new sheriff's office and jail facility." Land acquisition is a named purpose of the $96M bond — yet the actual site is being acquired now, from reserves, before any vote.

The most likely mechanism is reserve-then-reimburse: the County fronts the purchase from cash and, if the bond passes, reimburses reserves from bond proceeds. No document confirms this for this specific purchase; it is an inference. The County has done it before: the FY25 budget included "$1,044,000 Bond Proceeds for Affordable Housing" reimbursing an earlier reserve outlay. The May 6, 2026 draft ballot Options 1 and 2 expressly listed "refunding pre-development costs" as a bond purpose, which would have covered the $4.26M in pre-bond consultant spending already paid from current funds. The narrower July 2 draft names "acquiring land" but dropped "refunding pre-development costs"; whether the final adopted resolution (deadline Aug. 26) extends to this land purchase is unresolved.

The bond vote is a waivable contingency

The purchase agreement includes a bond-referendum contingency, but contingency (i) allows the County to waive it: passage of a referendum "may be released by Buyer and Buyer may elect to proceed to Closing notwithstanding, and at any time before or without, the holding of any such referendum." The County can close whether the bond passes, fails, or is never held.

At the public meeting, Supervisor Fixmer-Oraiz voted for the purchase as "a land option and not for any particular specific purpose." Chair Green described the jail as "the most likely outcome … regardless of what ends up being developed there, if anything." The executed contract warrants the County's ability to "use and develop the Property for its intended governmental purposes, including a County jail and sheriff's office." The purchase agreement is available for download on the Records page.

Price, assessed value, and the easement

The County is paying approximately $60,000/acre. The Iowa City Assessor's 2025 reassessment values the land at approximately $31,590/acre (all land; $0 improvements). The last recorded sale was May 13, 2021: $2,450,880 for the whole tract, implying roughly $60,000/acre if the parcel was approximately 40 acres at that time. Both figures are in the public record.

The agreement includes a 350-foot vegetative buffer easement, plus other easements and rights-of-way, counted in the gross acreage but limiting the area the County "may lawfully construct" on. The 35-acre figure is gross area, not buildable area.

The subdivision structure

The seller, IWV Holdings, LLC, owns a two-lot subdivision recorded as IWV Commercial Park. The County is buying Lot 1, which the agreement describes as the current Lots 3–8 of Melrose Commercial Park, to be replatted as Lot 1 of IWV Commercial Park. The seller retains Lot 2. Lot 1 is approximately 61% of the subdivision by area; Lot 2 is approximately 39%. The shared grading and detention-basin costs are split in that proportion. The detention basin sits on Lot 1 and serves both lots.

Costs and constraints beyond the purchase price

The $60,000 per acre is for gross land. The agreement's Land-Use Obligations article assigns the County additional costs and limits how much of the parcel can be built on.

- The 350-foot vegetative buffer easement encumbers part of the parcel and restricts construction within the buffer. The agreement states it may reduce the buildable acres. A 350-foot strip along one edge of the parcel would cover roughly 8 to 14 acres, depending on the final geometry.

- The stormwater detention basin is located on the southerly portion of the parcel, which removes additional land from the buildable area. The County pays not less than 61.04% of the cost to excavate and grade the basin. The basin serves both lots. The seller pays about 39% of that cost and provides no land for it.

- Master grading, the rough grading of Lot 2 and Lot 2 to the approved subdivision plans, is allocated to the County at not less than 61.04% of the cost, based on acreage. This is a floor, not a cap.

- The seller pays the full cost of extending sanitary sewer to Lot 2.

After the buffer, the detention basin, and internal roads and setbacks, the buildable area is likely in the low 20s of acres rather than 35. The 61.04% shares of grading and basin construction are separate from the $60,000 per acre. The exact buildable acreage and grading cost depend on the recorded plat and the approved subdivision construction plans, which have not been published.

The Iowa City Assessor lists the property as Class "C - Commercial," noted explicitly as "for tax purposes only. Not to be used for zoning." The purchase agreement requires Iowa City approval "including any necessary re-zoning and site plan approval" (contingency (j)) before closing. The parcel is inside Iowa City's corporate limits; the city holds full zoning authority.

The joint jail project collapsed in September 2025 when Iowa City's Mayor vetoed a proposed Riverside Drive site after a 4-3 City Council vote. The current purchase is contractually contingent on that same city's approval.

This parcel is immediately south of the Historic Poor Farm (4811 Melrose Ave, Iowa City), in the same far-western corridor the Board rejected as a jail site on April 22, 2026. Supervisor Sullivan cited "transportation challenges" among the reasons for that rejection. A bond rationale the County has cited is keeping incarcerated people near family — Bill Waldie (July 2, 2026): "so they're near their folks, near their family." No written transit or accessibility requirement for site selection has been identified in a primary source; this note will be updated if such a document is found.

Status Quo vs. New Facility

The Shive-Hattery analysis frames the choice as Build New (~$212M over 20 years) versus the forced-closure scenario (~$282M over 20 years). Neither scenario represents continuing to operate the existing jail.

The County FY27 budget projects continued operation of the existing jail with $800,000 in OoC overflow. Shive-Hattery's forced-closure scenario projects $4.8M/year average on the same line item — 6× the County's actual operating-plan figure — because the consultant assumes the jail closes and everyone moves out. The County is not planning to do that.

| Scenario | Annual cost basis |

|---|---|

| Current status quo (FY27 budget, function 1050) | ~$7.2M/year (incl. $800K OoC) |

| New facility — debt service only ($96M at 4.5%, 10-yr) | ~$12.13M/year |

| New facility — operating costs | Not published — no pro-forma operating budget has been released |

| New facility — all-in reference point (debt service + current JoCo operating at flat cost) | ~$18.5M/year ($12.13M debt + $6.4M operating — operating costs held flat at current $6.386M; no new-facility pro-forma available) |

| Forced-closure scenario / all OoC (annualized from 20-yr total) | ~$14.1M/year |

The new facility eliminates perhaps $440K–$800K/year in OoC costs while adding ~$12.13M/year in debt service (10-year term, June 10, 2026). The net debt-service burden relative to today is approximately $11.3–11.7M/year depending on whether the FY27 budgeted OoC figure ($800K) or the FY25 actual ($440K) is used as the baseline. Shive-Hattery has not published a pro-forma operating budget for the proposed facility, so the all-in annual cost cannot be calculated from available primary sources. As a reference point: if total operating costs held flat at the current $6.386M/year (most costs are personnel — you don't reduce staff simply because more people arrive), total annual cost would be approximately $18.5M/year ($12.13M debt service + $6.4M operating). Whether the new facility achieves lower per-person operating cost depends on assumptions that have not been disclosed.

The Shive-Hattery analysis does not present this comparison. The document's Build New figure (~$10.6M/year annualized at their $48.88M basis) already represents a ~47% increase over the current operating baseline — not a savings relative to today. At the MCIP's $96M, that annualized figure rises further.

Transport, Staffing, and Composition

Scope beyond the jail

The Shive-Hattery Vol I Needs Assessment (§IV.E / Appendix E) documents the full space program: a replacement Sheriff's Office, training facilities, courtrooms and offices for the County Attorney and other staff, and approximately 12,000 SF of Vehicle Maintenance and Storage for law-enforcement fleet repairs. Vol I does not reference the existing County Fleet Shop.

At the April 24, 2025 formal Board of Supervisors meeting (Granicus clip 3174), the Board passed a resolution for the "Fleet Shop Expansion Project, located at 4810 Melrose Avenue, Iowa City" — three additional bays, designed by Vantage Architects, estimated total cost $1,325,000, bids solicited May 15, 2025. The newly purchased jail parcel fronts Melrose Avenue (purchase agreement, access clause), placing the proposed new building across the street from the fleet shop just expanded. The proximity is verifiable on an aerial or parcel map.

Whether the two vehicle-maintenance programs serve distinct operational needs — for example, secure access for law-enforcement vehicles versus general county fleet — or overlap in function is not addressed in any published document. No cost breakdown separates the vehicle-maintenance program from the rest of the $96M.

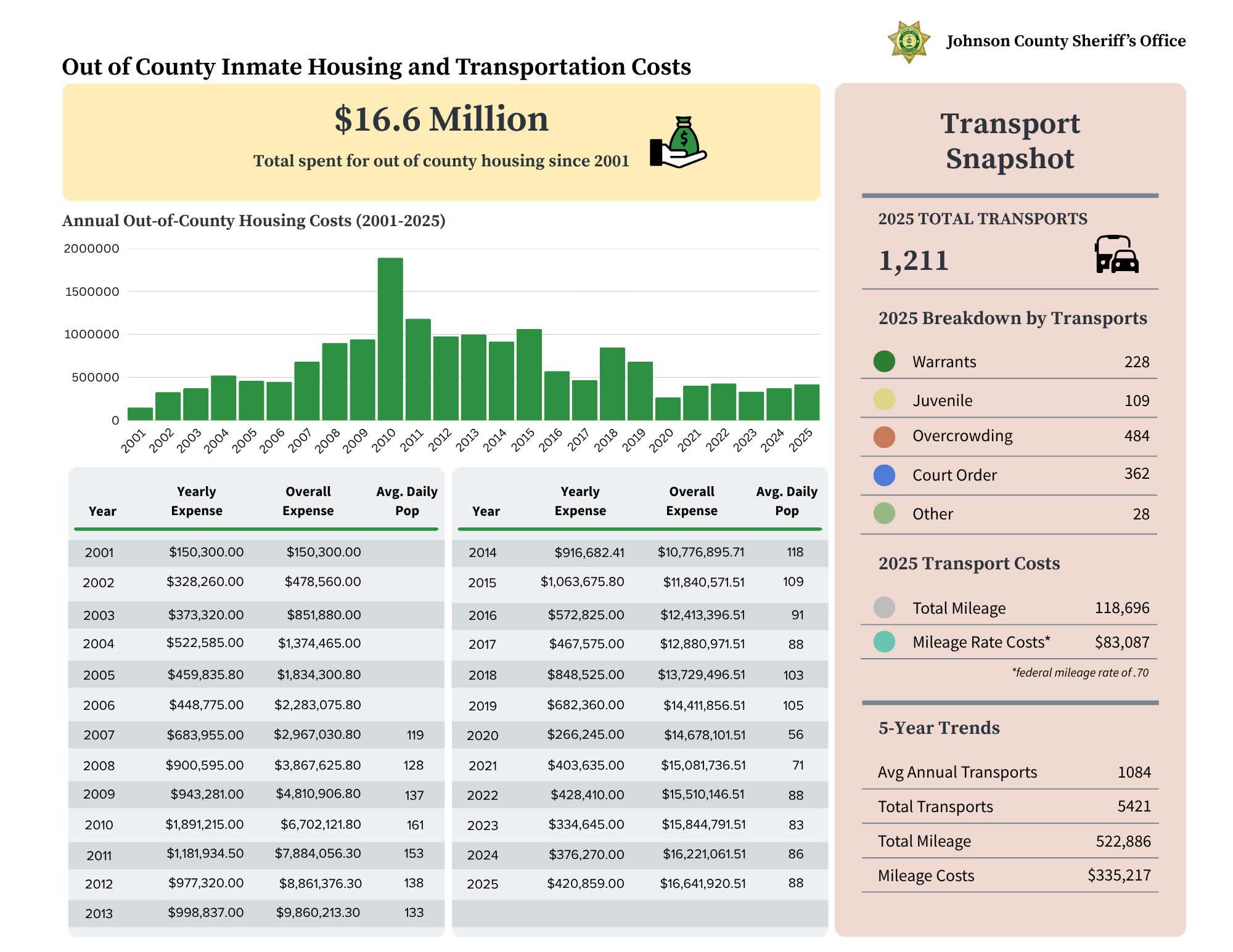

Overcrowding is a declining share of transports

The County's 2025 transport snapshot reports 484 of 1,211 transports (40%) as overcrowding-driven.

| Year | Total | Overcrowding | Share | Source |

|---|---|---|---|---|

| 2022 | 739 | 426 | 57.7% | Sheriff's FY26 Budget Presentation, slide 11 |

| 2023 | 827 | 383 | 46.3% | Sheriff's FY26 Budget Presentation, slide 11 |

| 2024 | 754 | 313 | 41.5% | Sheriff's FY26 Budget Presentation, slide 11 |

| 2025 | 1,211 | 484 | 40.0% | "Out of County Inmate Housing and Transportation Costs" infographic, 2025 |

The 2022–2024 data uses three categories (Jail Transfers, Mental Transports, Transport Court Order). The 2025 infographic uses five — adding Warrants (228) and Juvenile (109) categories that mechanically reduce overcrowding's percentage share without changing the absolute count. Overcrowding-driven transports peaked at 426 in 2022, fell to 313 in 2024 (a 27% decline), and rebounded to 484 in 2025 — tracking the Linn County contract ramp-up. None of this is broken out in the Sheriff's 2025 infographic.

The forced-closure scenario is sometimes read as a lean fallback. The staffing numbers say otherwise.

| Scenario | Staff | Role |

|---|---|---|

| Build New | 24 | Operate 140-bed jail |

| Forced-closure | 18 | Transport unit — transfer 83 people to other counties daily |

| Forced-closure | +12 | Operate intake/holding facility |

| Forced-closure total | 30 | 25% more than Build New |

Shive-Hattery describes these 30 positions as a minimum: "FTE's staff positions will increase as transportation growth occurs due to inefficiency and capacity issues of existing facilities." Those 30 positions cost ~$145M over 20 years — more than the $96.3M in OoC housing they exist to manage. Johnson County would also pay both the per-diem ($89.3M) and the transport logistics ($7M) as separate line items.

The document explicitly excludes liability from the model: "The scenarios projected do not consider the increased liability concerns associated with transporting people to other facilities. Liability is a significant factor for consideration in future evaluations, both for staff and incarcerated people." This is the only scenario-specific cost that carries a formal disclaimer.

FTE's staff positions will increase as transportation growth occurs due to inefficiency and capacity issues of existing facilities.

Is the 18 transport FTE estimate defensible?

The figure is stated in one sentence with no supporting breakdown. The current baseline, from the Sheriff's Programming Questionnaire (Vol I Appendix, p. 101), is four part-time transport drivers for a ~56-person in-house population with ~22 people held out of county. The forced-closure scenario calls for 18 FTE. The raw headcount rises from 4 to 18 (4.5×), but the comparison also involves a change in position type — from part-time to FTE — which typically carries a different cost structure. Neither the Vol I Appendix nor the Supplemental discloses the compensation basis for the current part-time positions or for the proposed 18 FTE: no hourly rate, salary range, or benefits eligibility is stated for either. The true cost difference between the current baseline and the forced-closure staffing model is therefore larger than headcount alone indicates, but by how much is not established in any published document.

An independent check using the NIC Staffing Analysis Workbook methodology — which Shive-Hattery itself uses for the Build New staffing calculation — yields a range of 15–22 FTE for a full-closure scenario with 83 ADP distributed across multiple counties, applying a standard two-officer minimum per vehicle (per ACA standards as incorporated in USMS Federal Performance-Based Detention Standards, and consistent with Shive-Hattery Vol. I staffing methodology) and standard single-watch shift relief factors. The 18 FTE figure falls within that range and is not obviously inflated. However:

- The population math is inconsistent: 18 FTE sized for 83 ADP, but $89.3M in per-diem implies ~170 ADP. If the document uses 170 ADP for the cost projection, transport staff would need to grow proportionally.

- Closer counties (Linn, Henry) are 30–55 minutes away. Lee County (Fort Madison) and Clinton County are 90–95 miles away — 3–4-hour round trips per Sheriff Kunkel's public statements (The Gazette). If closer counties fill up, the same 18 FTE cannot maintain the same transport volume.

- Linn County ended its U.S. Marshals agreement in part due to capacity constraints. A full-closure scenario requires guaranteed long-term contracts with enough combined spare capacity for all 83 people — an assumption the document treats as given.

Data Gaps

The following information would materially change the analysis if it were available and has not been published or produced in response to open-records requests as of July 2026:

- A final adopted bond resolution. The June 10, 2026 Board of Supervisors work session confirmed the ballot question as a $96M general-obligation bond for the jail and Sheriff's Office only; the resolution was deferred at the July 2, 2026 formal meeting (Granicus clip 3693); deadline August 26, 2026.

- The daily population count Shive-Hattery used to generate the $89.3M OoC per-diem projection. This is the load-bearing undisclosed variable in the $69.4M savings claim.

- The assumed bond interest rate in the Shive-Hattery Life Cycle analysis. Without it, the capital figures in the Build New scenario cannot be independently verified.

- A pro-forma operating budget for the proposed new facility. No such document has been released.

- OoC per-diem rate for Lee County. Rates for Washington ($60), Cedar ($65), Linn ($60), Henry ($60), and Clinton ($55) are known from Snapshot-26843 (slide 10). Lee County is the only OoC destination with an unconfirmed rate.

- The internal FY27 budget justification for the $800,000 SC349 (OoC housing) line — specifically, what calculation or policy decision drove the $160K cut from the decade-long $960K carry-forward. Sheriff Kunkel's FY26 budget presentation confirms the $960K figure predated his tenure; the FY27 worksheet offers only a reclassification note.

- Updated construction cost rates for the stand-alone $96M scope. Shive-Hattery's Vol I rates ($612/SF law enforcement, $800/SF jail, 2024) were developed for the joint facility. The August 2025 joint feasibility study updated rates for the combined scope, but no published document provides a stand-alone rate-and-scope buildup explaining the increase from $48.88M (Vol I) to $96M (MCIP).

- The composition of the MCIP's "Sheriff's Office Repairs" line: $600,000/year (FY27–FY29, Bond fund), described only as "Repair building as needed; annual monitoring." It is unclear how this relates to the Axiom stabilization scope documented in Part 4 ($3.23M–$3.365M), or whether the $600K/year represents a separate ongoing maintenance obligation on top of that remediation.

- A quantified projection of civilianization savings in the new facility's operating budget. The FY27 Budget Planning Information confirms the Sheriff is actively replacing sworn Detention Officer positions with civilian Corrections Officers at lower wages, but no pro-forma applies this trajectory to the proposed 24-FTE Build New scenario.

- Daily peak occupancy counts. The control-sheet data provides monthly averages (ADP), which understate the peak crowding episodes that drive transport decisions. Peak-day data has not been released.